By Luisa Maria Jacinta C. Jocson, Journalist

A RECOVERY to the government The spending helped the Philippine economy rebound in the third quarter, putting it on track to post Southeast Asia’s fastest growth this year.

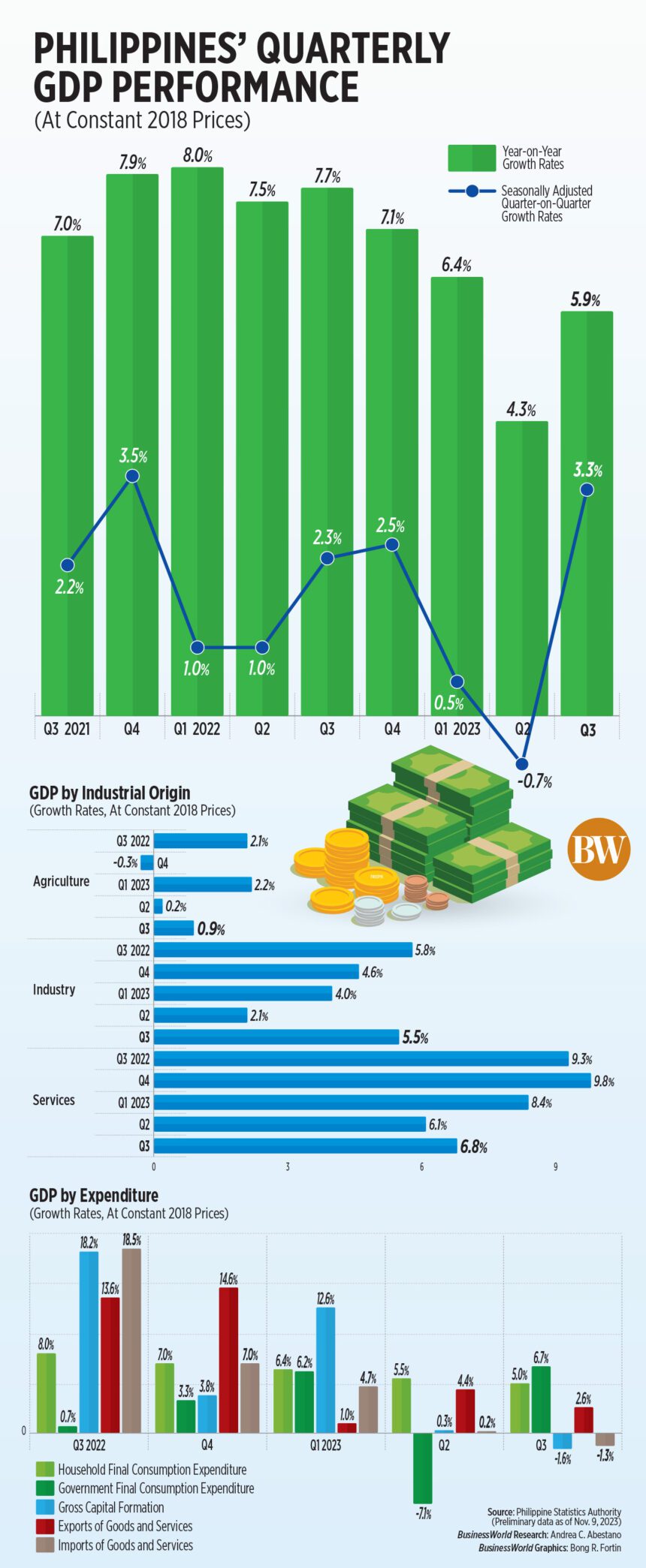

Preliminary data from the Philippine Statistics Authority (PSA) showed that the gross domestic product (GDP) grew 5.9 percent between July and September, faster than 4.3 percent in the second quarter but less than 7 .7% a year earlier.

This also exceeds the median estimate of 4.9% of 18 economists in a Business world poll last week.

The third-quarter expansion also ended three consecutive quarters of slowing growth.

The third-quarter expansion also ended three consecutive quarters of slowing growth.

The Philippines’ GDP growth in the third quarter was the fastest among major emerging Asian economies based on available data, National Economic and Development Authority (NEDA) Secretary Arsenio M. Balisacan said. , during a press briefing.Fing

With a GDP growth of 5.9%, the Philippines is ahead of Vietnam (5.3%), Indonesia and China (4.9%) and Malaysia (3.3%).

For the FiThe first nine months, economic growth averaged 5.5%, still below the government’s 6-7% target for the year as a whole.

“The economy will need to grow by 7.2% year-on-year in the fourth quarter of 2023 to reach at least the lower end of the government’s target,” Balisacan said.

On a seasonally adjusted quarterly basis, the Philippines’ GDP grew by 3.3 percent, a turnaround from the 0.7 percent contraction recorded in the second quarter.

The Philippines’ economic performance in the third quarter was driven by a recovery in government spending, which contributed to offweaken household consumption.

Government spending jumped 6.7%, faster than 0.7% a year ago and a turnaround from the 7.1% contraction recorded in the second quarter.

Mr Balisacan said catch-up plans by government agencies helped boost spending last quarter.

The PSA indicates that state spending contributed 2.1 percentage points to GDP growth, or the equivalent of 36%.

Household consumption, which made up about three-quarters of the economy, rose 5% in the third quarter, the weakest in two years. It’s also a slowdown from 8% a year ago and 5.5% the previous quarter.

“The slowdown in domestic demand is mainly due to the stronger rise in inflation. Now that we are able to reduce this inflation, we believe that domestic demand will improve this quarter and in the quarters to come,” Mr. Balisacan said.

A slight increase in inflation was observed in August and September, as food and fuel prices soared. In September, headline inflation accelerated to 6.1% from 5.3% in August.

PSA data showed that the main contributors to household spending were transport; miscellaneous goods and services; restaurants and hotels; housing, water, electricity, gas and other fuels; and education.

Gross capital formation – the investment component of the economy – fell 1.6%, ending nine consecutive quarters of growth. This is a reversal of the 18.2% expansion a year ago and 0.3% in the second quarter.

Mr. Balisacan explained that this was due to the substantial drop in inventories, as well as the slowdown in the durable equipment sector (1.75% compared to 10.5%).

“These offset faster growth in public construction, which increased 26.9% versus 0.7%, and private construction, which increased 5.1% versus 4.3%,” he added.

Exports of goods and services increased by 2.6% over the July-September period, a rate lower than the 13.6% a year earlier and the 4.4% of the previous quarter.

On the other hand, imports decreased by 1.3%. This is its first contraction since the first quarter of 2021. It is also a reversal of growth of 18.5% in the third quarter of 2022 and 0.2% a quarter earlier.

The rest of the world’s net primary income jumped 112.5%, more than 95.1% a year ago and 90.7% in the second quarter.

Gross national income, the sum of the country’s GDP and net income from abroad, increased by 12.1%. This figure is higher than 10.6% a year earlier and 8.6% in the previous quarter.

On the production side, all sectors showed growth in the third quarter. Services grew 6.8%, up from 9.3% a year ago, but faster than 6.1% in the second quarter.

“Services remain the highest share in total GDP in the third quarter of 2023 at 65.1%, which is higher than the 64.6% share in the same period of 2022,” the PSA said.

Industry growth slowed to 5.5% from 5.8% a year earlier. However, this increase was faster than that of 2.1% in the second quarter.

Agriculture, forestry and FiGrowth edged up 0.9%, less than 2.1% a year ago but better than 0.2% in the previous quarter.

“ALWAYS DOABLE”

Meanwhile, Balisacan remained optimistic, saying the government’s 6-7 percent growth target this year is “still achievable” and “still within reach.” However, challenges weighing on the outlook include geopolitical tensions and persistent inflation.

Any changes to the macroeconomic assumptions of the Development Budget Coordination Committee (DBCC) will also not be substantial.

“We will be close to most of the key assumptions, including GDP growth,” Balisacan said.

The DBCC will meet in December for its Fifinal review of objectives.

For the final quarter, Balisacan said a slowdown in inflation would help boost household consumption as the holiday season approaches.

“In October (inflation) is declining, so if we continue in this direction, we should be able to take advantage of revenge spending as a growth driver,” he said. “Inflation is the key to reviving robust consumption growth and hence the focus is on reducing inflation,” he added.

Mr Balisacan also said there remained a need to improve government spending and investment.

Security Bank Corp. Chief Economist Robert Dan J. Roces said in a Viber post that growth is expected to remain subdued in the coming quarters amid “cooling external demand and the impact high interest rates.

Makoto Tsuchiya, associate economist at Oxford Economics, said in a note that he expects growth to slow in the coming quarters due to the global economic slowdown.

“GDP rebounded strongly in the third quarter of the year, but we do not expect this strength to continue as high interest rates and slowing global growth will lead to further economic weakness over the coming quarters,” Gareth Leather, senior Asia economist at Capital Economics. , also said in a note.

In a note, ANZ Research said private consumption would continue to be the main driver of growth. However, he expects this situation to “weaken further amid slowing consumer confidence and stabilizing remittance income.”

BMI, a unit of Fitch Solutions, said it expects growth to remain stable in the fourth quarter. “Nevertheless, we believe the government’s projections of 6.5-8% in 2024 may prove a little too optimistic due to several headwinds,” he adds.

Nicholas Antonio T. Mapa, senior economist at ING Bank NV in Manila, said better-than-expected growth in the third quarter would leave more room for further tightening by the BSP.

“Robust growth coupled with hawkish statements from BSP Governor Eli M. Remolona, Jr., portends at least one more rate hike before the end of the year and perhaps two if inflation forecasts of the BSP for 2024 remain high,” he said in a note.

Mr. Mapa said the BSP would likely raise rates at its next meeting on Nov. 16 before raising them to 7 percent at its final meeting of the year in December.

Security Bank’s Mr. Roces warned that further tightening could dampen economic activity.

“This tightening of monetary policy, while essential for moderating inflation, carries the risk of slowing economic momentum, particularly in interest rate-sensitive sectors such as capital formation and consumer spending. With this, we believe the BSP will take a break in the next policy meeting,” he said.

Last month, the Monetary Board increased borrowing costs by 25 basis points (bps) in an off-cycle measure. This brought the benchmark interest rate to 6.5%, its highest level in 16 years.

The BSP has raised interest rates by 450 basis points since May 2022 to fight against inflation.

The central bank said in a statement on Tuesday that it would “keep monetary policy settings sufficiently tight untilflinflation expectations are better anchored and a downward trend sustained inflation becomes obvious.